Buy utility knowledge is now under 2008 ranges! However I would like to clarify why this stage has extra in frequent with 2014 housing knowledge than the credit score stress markets of 2005-2008, and why you must care. Understanding this knowledge line and what it’s making an attempt to inform you may be extra invaluable than erroneously pondering the market is crashing and we’ll see a wave of foreclosures.

Within the earlier enlargement, one among my long-term calls was that the MBA buy utility knowledge won’t ever hit the amount stage of 300 till the years 2020-2024. Credit score development within the earlier enlargement was going to be gradual and regular till our family formation knowledge bought excessive sufficient to get demand larger. Proper on cue, 2020 got here and we hit the 300 stage.

The years 2020-2024 have been going to be the time when whole house gross sales might lastly attain 6.2 million, one thing that couldn’t occur from 2008-2019 as a result of we didn’t have the demographic profile to get to that stage till family formation grew.

Nevertheless, the housing market did run into one drawback in 2020. Stock ranges broke to all-time lows and thus created large housing inflation shortly, which broke my mannequin. I knew housing could be OK so long as house costs solely grew at 23% over 5 years — 4.6% nominal per 12 months at most. We’re up 43% since 2020.

In the summertime of 2020, I talked about how the housing market would change, nevertheless it wanted the 10-year yield to interrupt over 1.94%, which roughly means 4% plus mortgage charges. That occurred in March of this 12 months. With the large housing inflation since 2020 and better mortgage charges, we’re again to acquainted territory with present house gross sales and buy utility knowledge: we’re again to 2014 ranges.

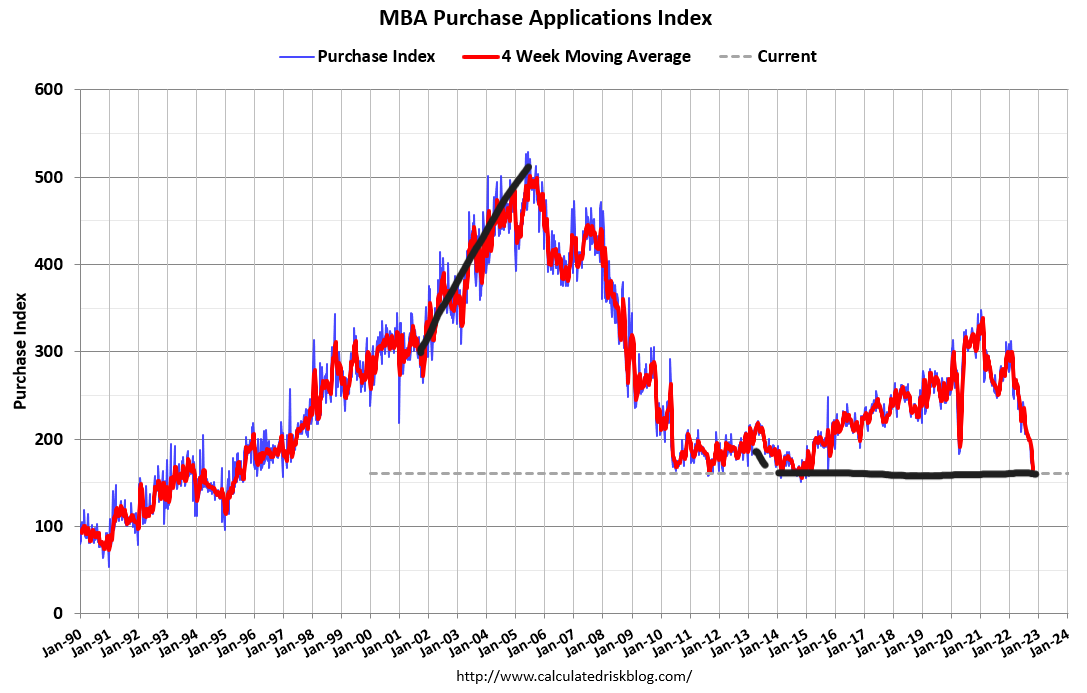

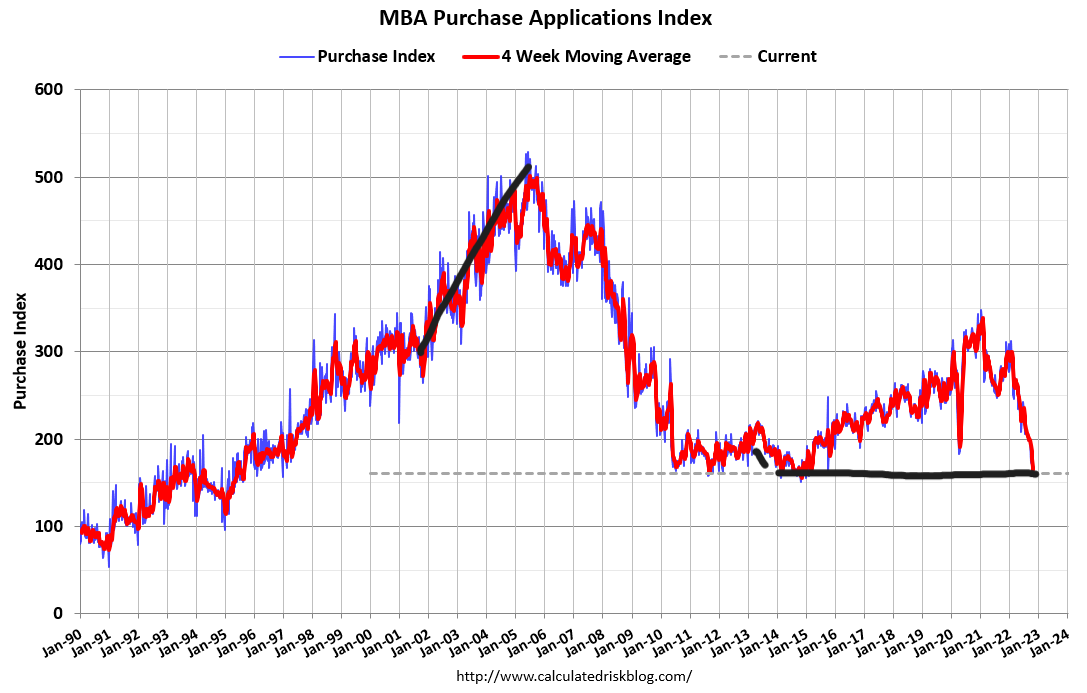

Wednesday’s buy utility knowledge was up 1% from week to week. It’s been in a variety of -2% – +1 % for a while now, not counting the hurricane week in Florida. The year-over-year knowledge is down 41%, and the four-week shifting common is 40.25%.

For a while now, I’ve been speaking about how the year-over-year comps will get difficult beginning in October of this 12 months, and this could imply buy utility knowledge can be down 35%-45% throughout this era; that might be the norm. Because the begin of October, the year-over-year declines have been in a variety of 39% -42% every week.

The information seems to be right. If we had one other leg decrease in demand, the acquisition utility knowledge goal could be down by 53% to 57%. We haven’t seen that within the knowledge but.

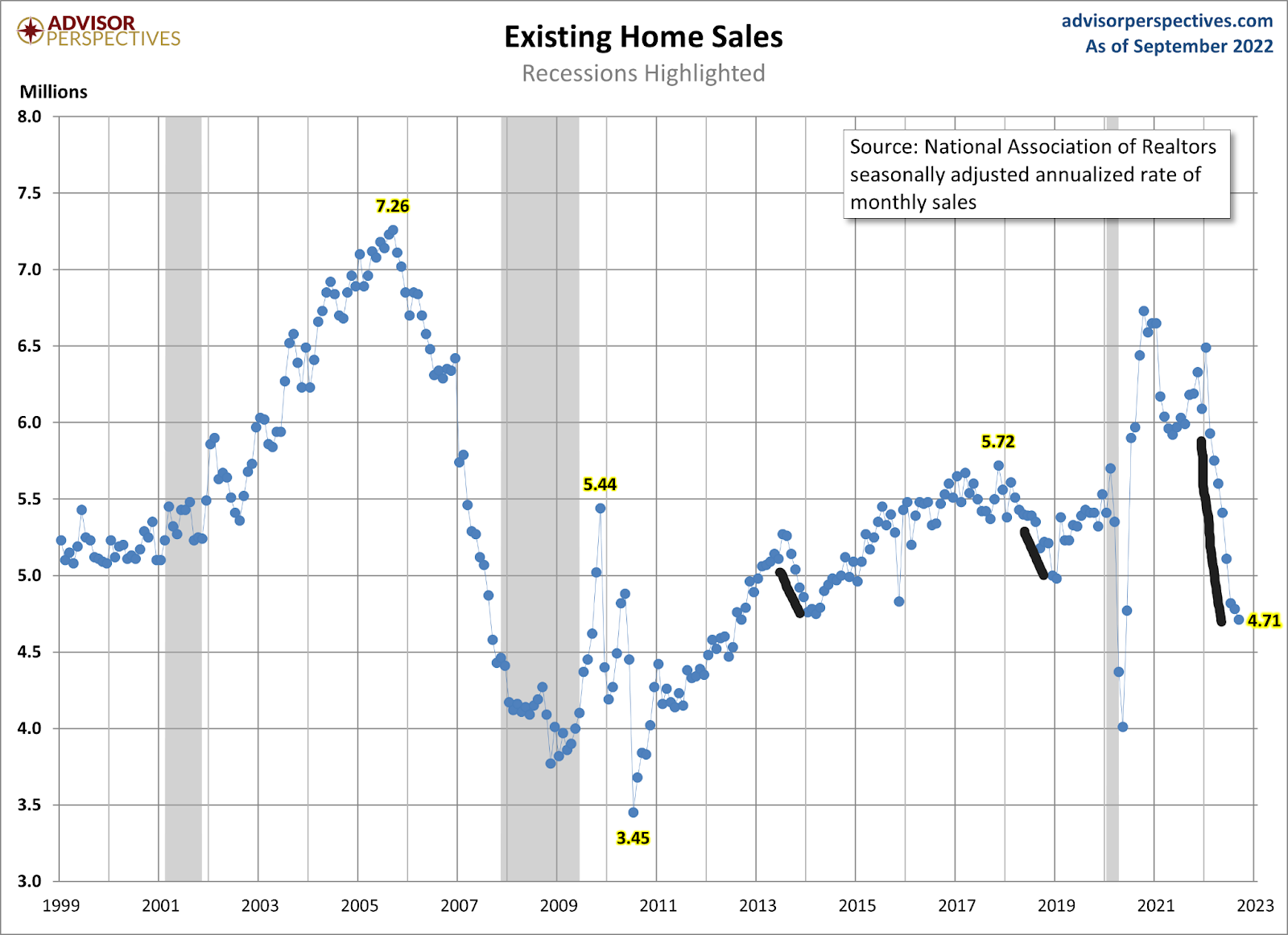

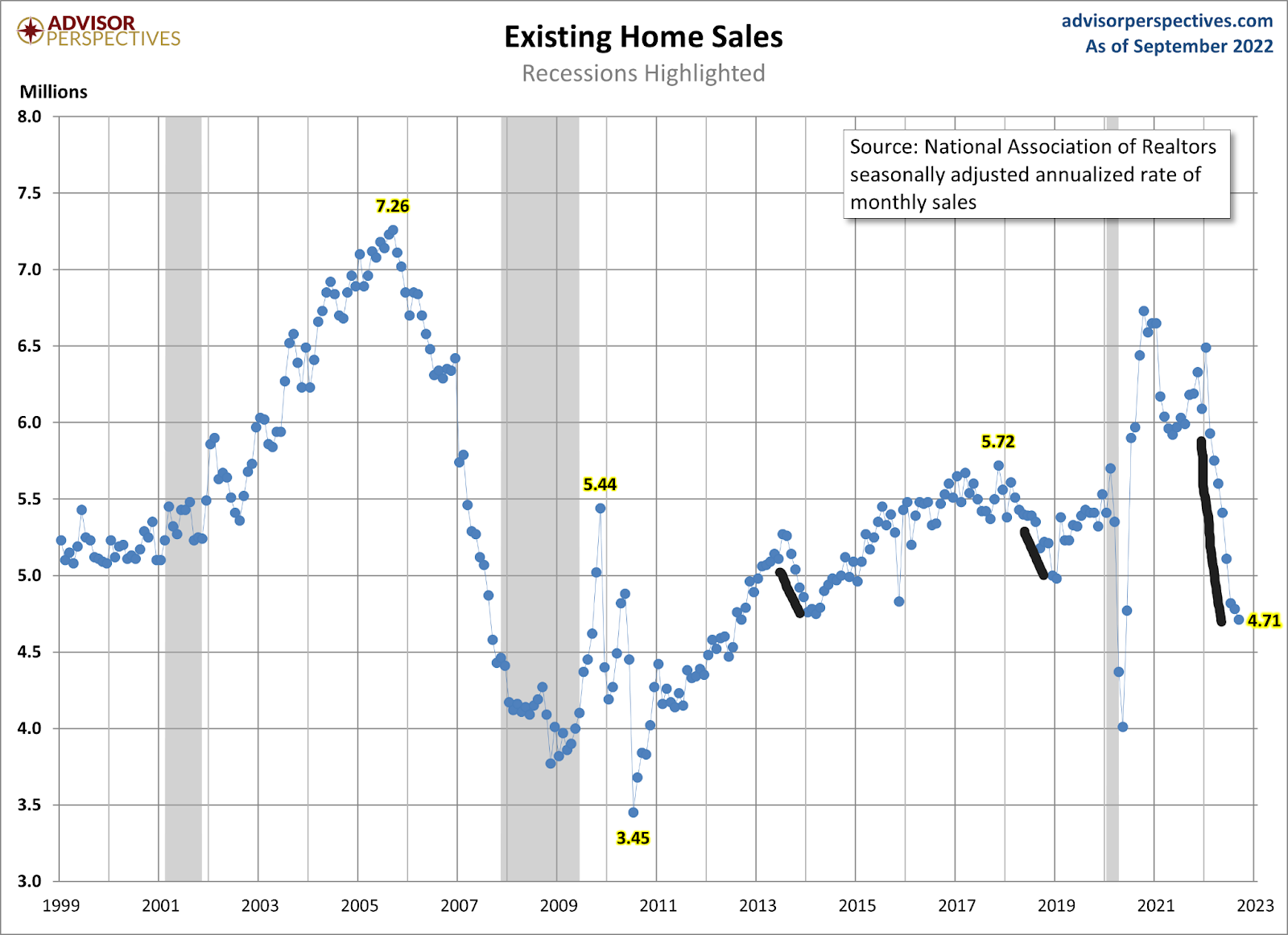

Wanting on the chart under, buy utility knowledge is under 2008 ranges immediately, very near the lows we noticed again in 2014, which, adjusting to inhabitants, was the bottom stage ever. This time round, we’ve not seen the form of housing credit score growth that we did from 2002-2005.

Submit-2012, each time mortgage charges rise, present house gross sales at all times development under 5 million. We noticed this occur in 2013-2014 and 2018-2019. Nevertheless, now with the historic worth inflation we’ve seen since 2020 and the large will increase in mortgage charges because the begin of the 12 months, we’ve the largest housing affordability hit of our lifetime in a brief period of time.

Buy utility knowledge is again towards 2014 ranges, and present house gross sales have trended again to 2014. Mortgage charges are larger now than again then, and the value beneficial properties are extra large.

The obvious distinction between now and 2014 is that whole stock ranges are roughly 1 million decrease now than the height of 2014. Again then, the height was roughly 2.3 million; immediately, it’s 1.25 million. Owners are in a greater monetary state of affairs now, they reside of their properties longer and longer, so the stock channels have been a lot completely different post-2012.

NAR whole stock knowledge 1,250,000

One factor about buy utility knowledge and demand is {that a} conventional vendor is often a purchaser of a house. Because the finish of June, we’ve seen that the house vendor referred to as it quits earlier this 12 months than standard, and now the brand new itemizing knowledge is detrimental 12 months to this point. This implies much less demand for housing.

New itemizing knowledge is down 5% 12 months to this point, as you may think about. With charges spiking as they did, it isn’t interesting for some individuals to promote their properties and purchase one other observe. Some individuals merely can’t transfer as a result of they’ll’t afford to.

I nonetheless imagine this influence on demand isn’t getting the eye it deserves. This occurred on the finish of June when the housing recession additionally began. We haven’t had 12 months of knowledge but with this actuality. New itemizing knowledge should develop 12 months over 12 months within the spring of 2023, or else the mortgage fee lockdown dialogue will get louder.

It’s a first-world drawback; householders are in excellent monetary form and management of their lives, in contrast to what we noticed from 2005-2008. Nevertheless, it’s not a great factor for housing demand when new itemizing knowledge is declining once we began 2022 on the lowest stock ranges ever.

That knowledge seems to be even worse when adjusting to inhabitants and households. Historically, stock ranges have been between 2 million to 2.5 million. As we are able to see, the housing bubble crash was an irregular historic interval, identical to what we’re coping with immediately.

NAR Complete Stock knowledge 1982-2022: Most Current Report

As we are able to see, buy utility knowledge is absolutely under 2008 ranges, and present house gross sales have trended again to 2014 ranges, the final time buy utility knowledge was detrimental. Buy utility knowledge adjusting to inhabitants in 2014 was the bottom stage ever recorded and we nonetheless had over 5 million whole house gross sales again then.

Housing affordability, whereas not in a disaster earlier than 2020, bought into main bother with worth escalation since 2022. This is the reason affordability and a scarcity of recent listings needs to be the main target for housing as a result of these two are the actual demand hits proper now.

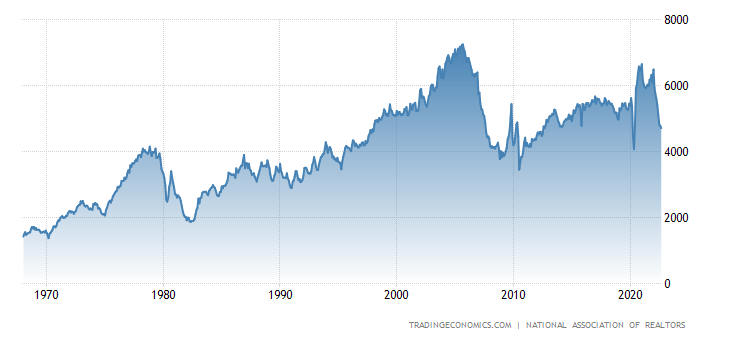

It’s uncommon post-1996 to have present house gross sales traits under 4 million. It actually solely occurred in 2008 after a serious housing crash and credit score dried up. The COVID-19 pause despatched gross sales all the way down to 4 million however we simply shot proper again up

NAR: Current House Gross sales At the moment 4,710,000

Credit score isn’t going to dry up because it did from 2005 to 2008, as a result of it’s principally a 30-year fastened mortgage mortgage we’re offering lately. Nevertheless, we do have to see new itemizing development choose up subsequent 12 months to have a extra purposeful housing market.

Nevertheless, with the affordability hit we’ve immediately with charges over 7% and the dearth of recent itemizing development, which means fewer sellers who would-be patrons, we are able to get again all the way down to 4 million and underneath if these traits proceed. The purpose of this text is to indicate you the dramatic influence of upper charges and costs and that we have to focus extra on the brand new itemizing knowledge, which all of us ought to wish to improve.

{kind=link}