[ad_1]

Financial studies over the Thanksgiving vacation paint an advanced image of what’s taking place, and the place we’re on recession watch. The massive financial shock was the energy of Black Friday gross sales, the place customers spent a report $9.12 billion on-line. One other shock was the Atlanta Fed’s forecast of 4.3% GDP development within the fourth quarter, because the Atlanta Fed information was utilized by many to say that the U.S. went right into a recession earlier within the yr.

The roles information, nonetheless wasn’t a shock: the unemployment fee is now 3.7% and jobless claims are nonetheless very low traditionally.

With all the information we now have in entrance of us, we will say that the U.S. didn’t go right into a recession firstly of 2022. The query now’s whether or not there’s a method to keep away from the job-loss recession we’re going through in 2023.

The U.S. housing market went into recession in June of this yr, which I talked about a number of months in the past on CNBC. A recession signifies that gross sales and manufacturing are down. New and present dwelling gross sales are falling, together with housing permits and begins, as we have now too many new houses for the builders to subject new permits.

The job loss recession is already right here within the housing market, and whole incomes are falling with much less quantity on this sector. Though we don’t have this within the bigger economic system but, housing historically will get weaker right into a recession as it’s a rate-sensitive sector of our economic system.

The Federal Reserve has forecast a 4.4% unemployment fee subsequent yr, which might imply an instantaneous 1% enhance from the cycle lows within the unemployment fee, which once more implies the job loss recession is one thing they’re in search of (I’d even say need).

Why do they need a job loss recession? Their primary aim is to deliver down inflation, and People dropping their jobs is the quickest method to create extra labor provide and weaker demand. Accordingly, I raised my sixth (and final) recession purple flag on Aug. 5.

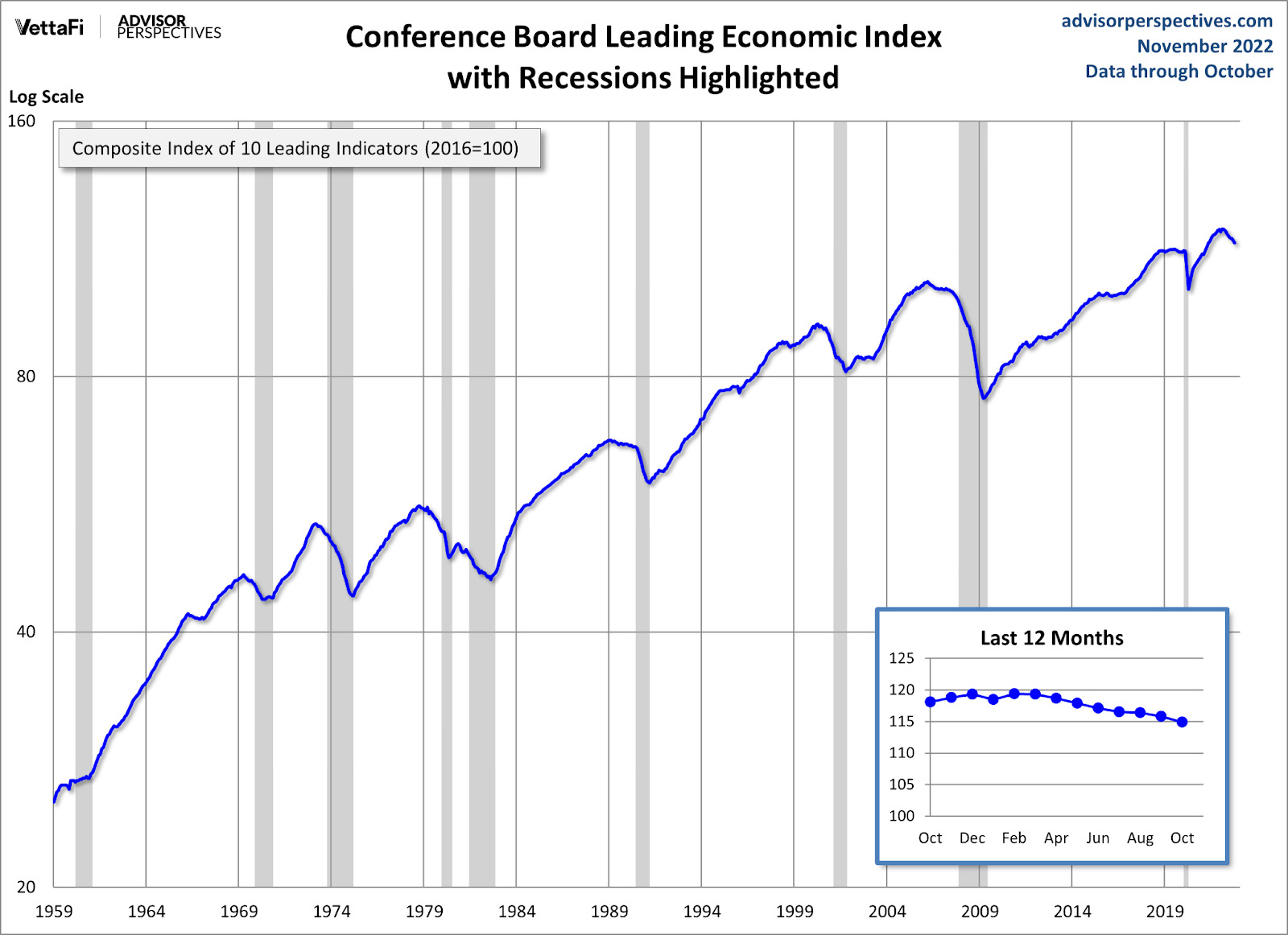

It was obvious on Aug. 5 that the main financial index was in a downtrend that’s much like each single recession we have now seen for many years. The latest main financial index report has confirmed that the downtrend within the information continues to be intact.

I mentioned this with the Convention Board earlier this yr as I offered my six recession purple flag mannequin to them. As all the time, with any index, you have to know the elements and their weighting and perceive how these elements will look sooner or later.

“The US LEI fell for an eighth consecutive month, suggesting the economic system is probably in a recession,” stated Ataman Ozyildirim, senior director of economics, at The Convention Board in November. “The downturn within the LEI displays customers’ worsening outlook amid excessive inflation and rising rates of interest, in addition to declining prospects for housing building and manufacturing.

So with all these components in place — housing already in a recession, the Fed’s current actions and coping with inflation — can we keep away from this job loss recession? Sure, we will. Will probably be onerous, and we are going to want a number of assist, however there’s a pathway to this.

Two issues have to occur

1. Inflation development fee and lengthy bond yields have to go down collectively.

The Fed is bent on driving us right into a recession to make it simpler to realize their single mandate to deliver down inflation. We have now already seen a few of the development charges of inflation falling.

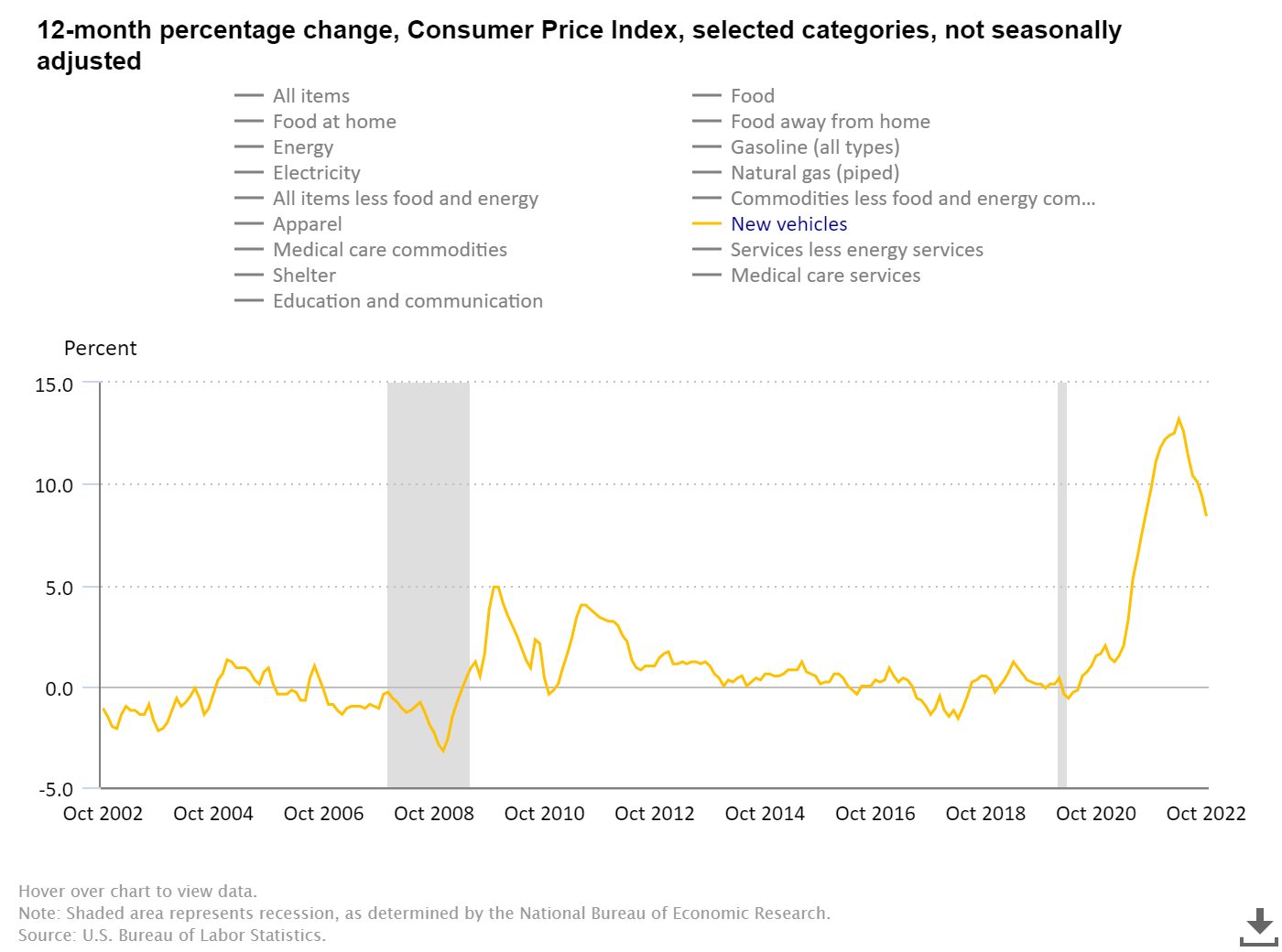

The used and new automotive value development fee is falling. As you all know, automotive manufacturing was horrible in the course of the world pandemic, and we’re working our means again to some sense of regular in auto manufacturing.

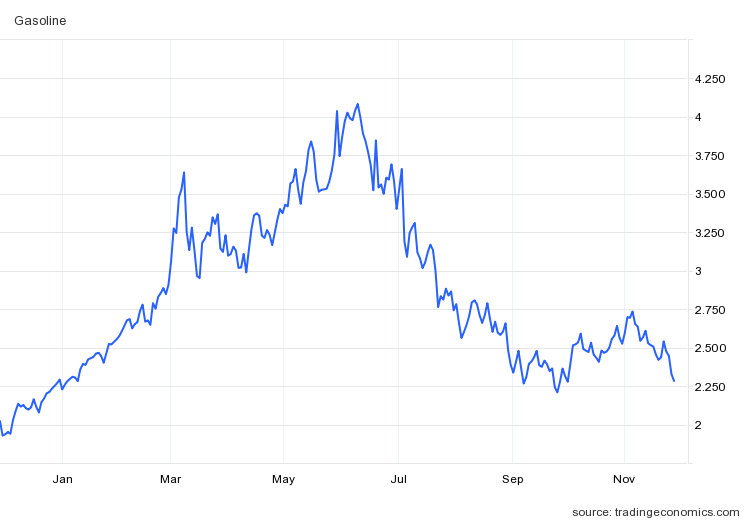

Gasoline costs are additionally falling. We have now a number of variables right here which can be out of our management that make this sector a bit irregular right now, together with the Russia wild card, releasing a lot of strategic reserves, and OPEC’s view of us. Nevertheless, for now, fuel costs are down.

As well as, costs paid for transportation of merchandise from China to the U.S. are falling from the COVID-19 peaks. China’s economic system is in horrible form with fixed lockdowns. Nevertheless, with much less demand for items from China, we’re receiving much less stuff and our port backlogs are resolving as we have now turn into a bit extra environment friendly on the ports.

We used to have tons of boats within the waters of the Pacific ready to be docked to take stuff to the shops. Now, this hectic side of transportation prices is gone and the concern of a downturn within the freight trade is taking maintain.

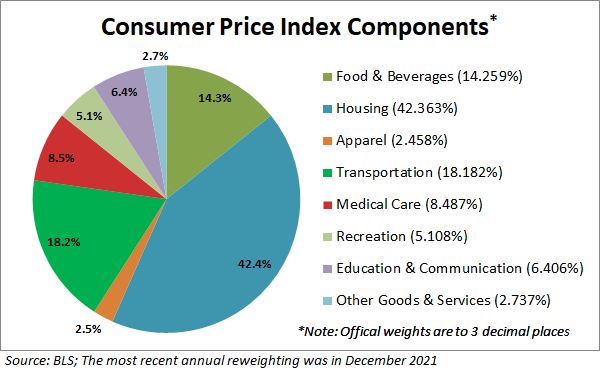

Nevertheless, the largest element of inflation isn’t the transportation value of products from China to the U.S., it’s hire shelter inflation, which makes up 42.2% of the patron value index.

Housing is the numerous X think about our economic system; I imagine the expansion fee of shelter inflation is already cooling off, it simply gained’t get picked up on the CPI date till subsequent yr.

In September, when the CPI inflation information was being reported on, I talked with CNBC about how this information line lags with the CPI information. As well as, we have now a number of two-unit building constructed, which is able to deliver extra provide on-line.

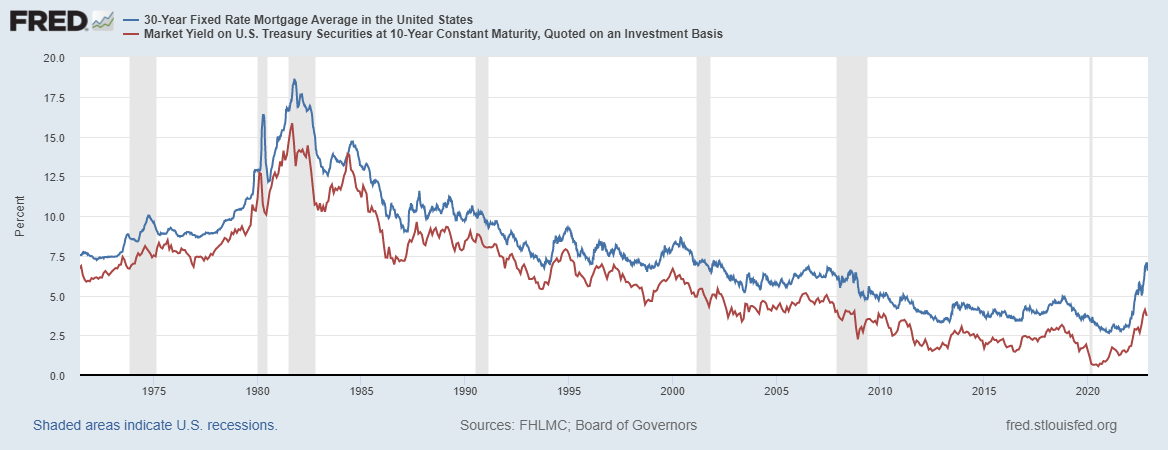

If we will get this to occur, the Fed can finish their fee hikes as soon as they get to their desired degree over the following few months. If the bond market’s lengthy finish can fall, we will get mortgage charges again down to five%.

Why does 5% matter?

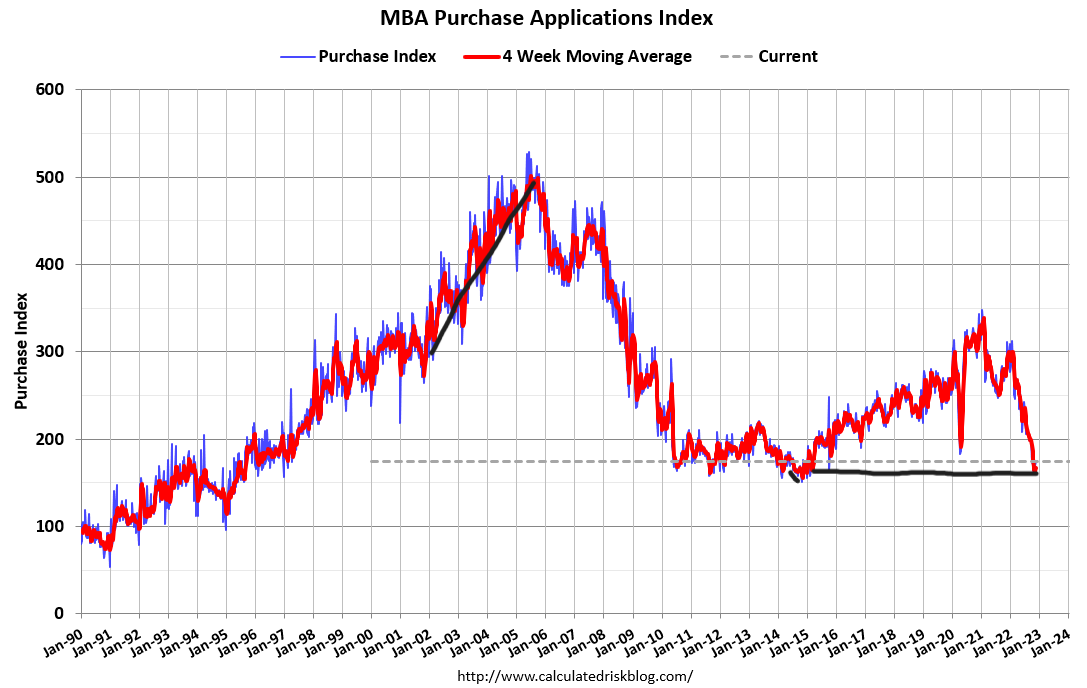

At the moment, charges have fallen from 7.375% to 6.62%, which has boosted the weekly demand information to be optimistic for 3 weeks. Final week we had a decline within the year-over-year unfavourable information, which went from 46% year-over-year declines to 41%.

Bear in mind, an enormous speaking level of mine is that we’d have onerous comps beginning in October of this yr on a year-over-year foundation. Final yr, buy utility information quantity was rising late within the yr, which was irregular. I’ve talked about having 35% to 45% year-over-year declines because the norm from October to January, with a doable 53% to 57% decline if demand will get worse. Properly, since October, the year-over-year declines have been between 39%-46%.

If mortgage charges maintain going decrease and we get extra weekly information development, we do have to see a noticeable year-over-year decline to warrant speak of stabilization. Proper now we’re working from a shallow bar, so we have to present context with the current strikes in buy utility information.

The housing market getting some stabilization can be a plus as we noticed some consumers come into {the marketplace} with charges at 5%. Charges additionally want to remain at that decrease for longer as effectively. What can’t occur is mortgage charges above 7%, since that degree hasn’t fueled new listings, which implies much less demand, and the builders merely are completed constructing something new with charges that prime.

Nevertheless, getting mortgage charges decrease with length will assist housing. The one subject right here is that whole stock ranges in America are nonetheless traditionally low, and the Fed doesn’t need dwelling costs to blow up larger. This may stop them from aiding housing in any significant means due to the concern of what we noticed in 2020 and 2021; it was savagely unhealthy.

NAR whole stock information: 1,220,000 listings

The important thing right here is that if the expansion fee of inflation falls and mortgage charges can get again towards 5% with some length, that may cease the bleeding within the one sector of the economic system that’s in a recession. Additionally, decrease mortgage charges means these households that purchased houses with larger charges lately can refinance if they will qualify.

2. The Fed pivots early when the labor market begins to get unhealthy

Fed Chairman Powell could have a talking engagement this Wednesday, so we’d have the Grinch for Christmas speech about how People have to really feel extra ache for his jolly Fed members to get their job completed taking down inflation. Apart from that, I don’t imagine the Fed pivots till the roles market begins to interrupt.

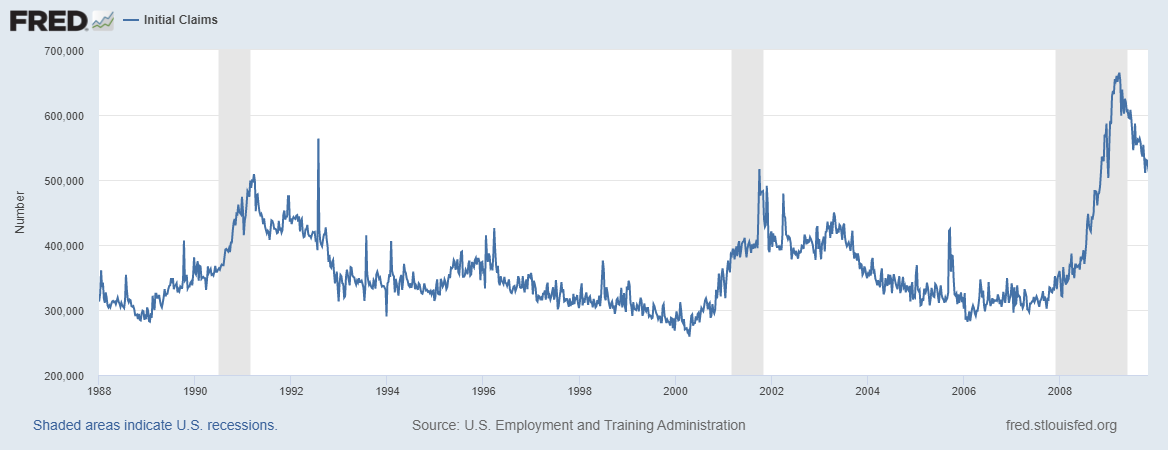

My goal for the Fed pivot is that jobless claims break above 323,000 on the four-week shifting common. The final headline print got here in at 240,000, so we aren’t near breaking over that quantity but on a four-week shifting common.

This degree isn’t a excessive degree traditionally after we have a look at jobless claims information. Nevertheless, contemplating how low we obtained in jobless claims at 166,000 and the place the job openings information is at the moment, if we break above 323,000, the Federal Reserve will get its beloved job loss recession as a result of as soon as jobless claims break, the downturn has simply began.

The chart beneath exhibits preliminary jobless claims and the shaded gray components outline after we are in a recession. The chart exhibits the final three recessions, not together with the COVID-19 recession. As you’ll be able to see beneath, when jobless claims have an aggressive rise working from a low degree, the job loss recession is occurring.

If the Fed can pivot and present that they’re as soon as once more a twin mandate Fed, which implies they care about employment, then the injury is completed early on and might be acted on rapidly by the Fed.

That is the place it will get difficult because the Fed has talked about not chopping charges when the economic system will get weaker and has harped on People feeling extra ache for his or her job to be completed. For now, the sturdy stability sheets of American households have saved consumption going. However, as short-term charges rise, People will really feel it on their bank cards, dwelling fairness strains, and any mortgage charges which have recast.

The Fed believes the energy of the U.S. client offers it some cowl to hike charges aggressively. Up to now, I agree with the Fed; the patron stability sheets look good, however you shouldn’t depend on your prime horse to win each time.

We hear a number of discuss recession. As well as, we all know housing is in a downturn, manufacturing information is wanting weaker, the worldwide economies are struggling, China is a big mess, Europe is coping with an financial struggle with Russia and even my six recession purple flags are raised. Historical past has proven us time and time once more {that a} recession isn’t that far-off when a number of these information strains flip unfavourable collectively, all with the Fed elevating charges.

Nevertheless, what we have now right here in America is totally different than different international locations; we’re the one financial superpower on the earth. We have now strong family stability sheets and a large younger workforce that may exchange older employees and eat items and providers.

We mounted a few of the financial sins of the previous and had the longest financial and job growth in historical past earlier than COVID-19 created a short recession. We recovered from that recession rapidly when so many individuals stated we’d be in a despair after that occasion. A few of these components that satisfied me that we’d get better in 2020 are nonetheless right here.

The final time I had all six of my recession purple flags was late in 2006 and we had a large client credit score bubble brewing that arrange the good monetary recession. However we don’t have that this time.

Sure, historical past isn’t on our facet, however typically we create our historical past as we did with America is again financial restoration mannequin. With some assistance on the availability facet we will have shelter inflation go down, as a result of the easiest way to battle inflation is to create extra provide, not by destroying demand. We have now to keep in mind that we have now over 900,000 plus two-unit housing beneath building that ought to get on-line subsequent yr which is able to assist with rental inflation.

Then we want the Federal Reserve to get off the Grinch of Christmas theme of inflicting extra ache for People by jacking up charges and having banks earn more cash on their bank card curiosity costs. If lengthy bond yields fall, mortgage charges will fall with them prefer it has since 1971.

If that occurs and mortgage charges can get towards 5%, then the housing market can discover some stabilization and the bleeding can cease. So, we do have a method to keep away from a recession, and regardless that historical past isn’t on our facet at this stage of the financial growth, we will join the dots right here and chart a path that avoids extra ache.

[ad_2]

Source link